Usage-Based Car Insurance in India 2025 has become a mainstream choice for car owners, changing how premiums are calculated. Unlike the old system, every driver had to pay a fixed annual amount. This was regardless of how much they used their car. This model allows premiums to be linked directly to driving behavior. If you drive less and drive carefully, you pay less. If your driving is riskier or you’re on the road constantly, your premium reflects that too. This shift makes insurance fairer because it finally considers individual usage rather than applying a blanket cost to everyone.

What exactly is Usage-Based Insurance (UBI)?

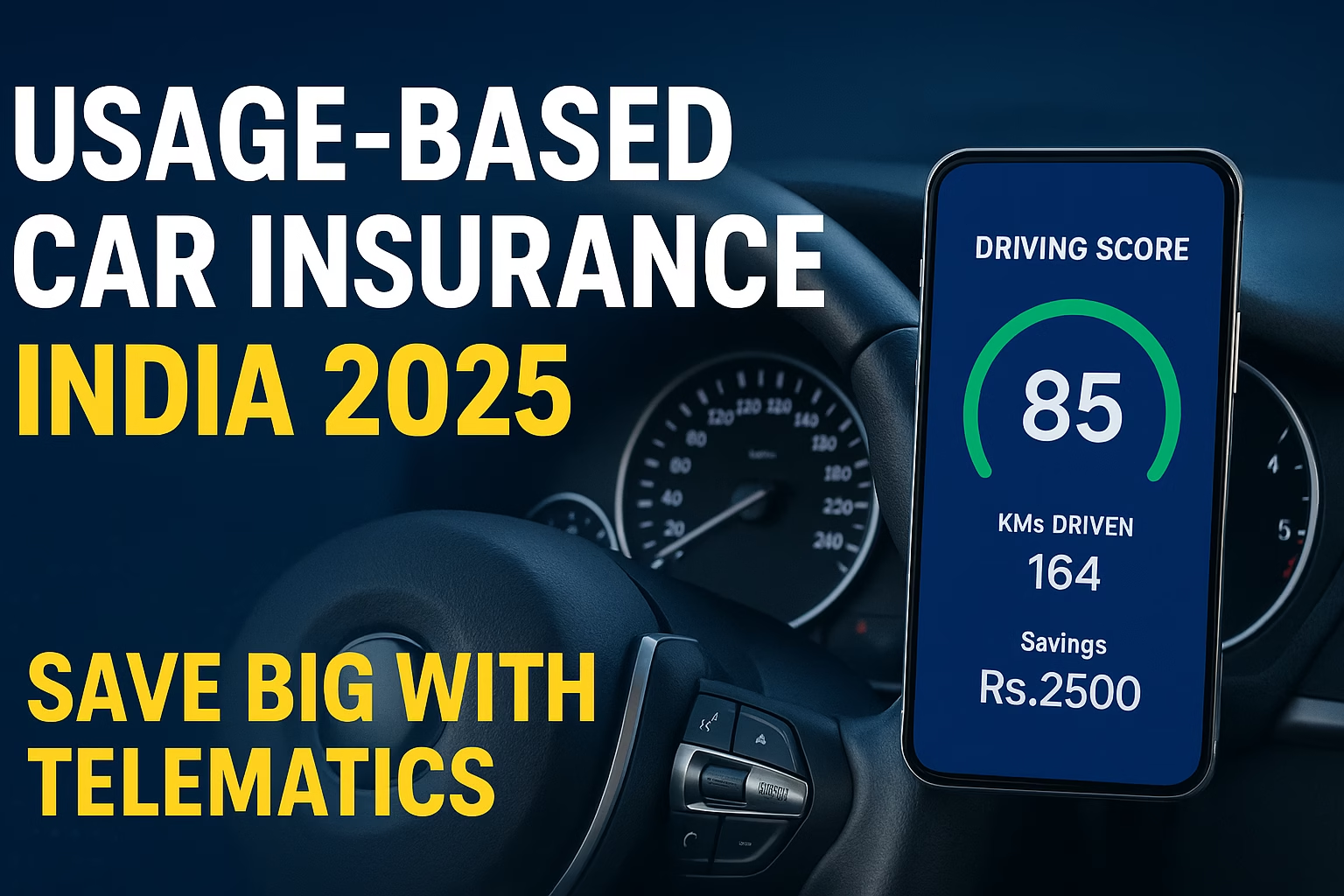

UBI goes by names like Pay-As-You-Drive and Pay-How-You-Drive. The idea is simple: the data collected about your driving is translated into a score. Safer driving and fewer kilometres usually mean a lower premium. The framework for such products has been enabled by the regulator, so insurers can offer these legally in India.

👉 For official guidance and circulars, visit the IRDAI website.

How telematics works (without the jargon)

- Device or app: Your insurer provides an OBD device or a mobile app to record trips.

- Data captured: Kilometres driven, acceleration and braking patterns, typical travel time, and sometimes location context.

- Scoring and pricing: Your profile updates in the background. Consistently safe driving unlocks lower premiums at renewal or even during the policy term (depending on the insurer’s design).

Who actually saves with UBI?

UBI isn’t only for enthusiasts. It makes practical sense if you:

- Drive under 8,000–10,000 km a year (WFH, short commutes, or a second car).

- Mostly drive during the day on city roads and avoid aggressive manoeuvres.

- Want more control over pricing and are comfortable with app-based feedback.

Quick example: A Pune family keeps one hatchback for errands and weekend trips, doing ~500 km a month. Their premium dropped by about 25% after switching to a kilometre-slab UBI plan and maintaining a high safety score.

Benefits you’ll notice right away

- Fair pricing: You aren’t subsidising high-risk drivers. Your behaviour sets your rate.

- Real savings for low mileage: If the car sits idle most weeks, why pay a commuter’s premium?

- Coaching nudges: The app highlights hard braking or speeding spikes so you can improve.

- Trip transparency: See exactly how your driving affects your cost.

- Good habits stick: Safer driving reduces accident risk and maintenance surprises.

Trade-offs to think through

- Privacy: Some drivers don’t want trip data collected. Read the insurer’s data policy before you opt in.

- Tech reliability: Phone GPS or OBD devices can glitch. Report issues early so your score isn’t affected.

- High-mileage drivers: If you routinely exceed 15,000 km a year, UBI is not be cheaper than a regular plan.

- Availability: While expanding, some cities or variants still be limited.

UBI vs traditional car insurance (at a glance)

| Factor | Traditional | Usage-Based (UBI) |

|---|---|---|

| Premium logic | Vehicle profile + geography + age | Driving score + kilometres + vehicle profile |

| Best for | Daily commuters, high mileage | Low-mileage, smooth drivers |

| Transparency | Fixed, fewer levers to change | Dynamic, feedback-driven |

| Gear needed | None | App or OBD device (simple setup) |

| Availability | All insurers nationwide | Growing list of insurers and cities |

What to check before you buy

- Type of plan: Some are kilometre slabs (buy 5,000/7,500/10,000 km). Others focus on behaviour (safety score-linked).

- Add-ons still matter: Zero Depreciation, Engine Protection, RTI and Roadside Assistance remain valuable—UBI affects pricing, not coverage basics.

- Data policy: Confirm who can access your driving data and for how long. Opt out if you’re not comfortable.

- Exceeding kilometres: Understand top-ups or per-km charges so there are no surprises mid-term.

- Claim process: UBI should not complicate claims. Ask how the insurer handles disputes about trip data.

Indian context: why UBI is trending now

Urban driving patterns have changed. Many households mix public transport, cabs, and occasional personal car use. Insurers are responding with flexible pricing to match actual usage.

👉 For broader market moves, check the Economic Times Insurance Section.

FAQs

Q1. Is Usage-Based Car Insurance approved in India?

Yes. The regulatory framework permits telematics-based products. For policyholder advisories and circulars, refer to the IRDAI website.

Q2. Do I need to install a gadget in my car?

Most plans work via a smartphone app or a simple OBD device. Setup is quick, and support teams can help if you get stuck.

Q3. Will UBI affect my No Claim Bonus (NCB)?

NCB rules remain the same. If you don’t raise a claim, your NCB accrues as usual—UBI only changes how the base premium is calculated.

Q4. What if I exceed my kilometre limit?

You can usually top up kilometres or move to the next slab. Check rates ahead of time so you aren’t surprised.

Q5. I drive a lot for work. Will UBI still help?

Probably not. If your annual mileage is high or your safety score fluctuates, a standard comprehensive plan may cost less overall.

Q6. Is UBI useful for EV owners?

Yes. Connected EVs already capture rich telematics, which makes scoring cleaner. Pair UBI with Battery/EV-specific add-ons for best results.

Bottom line

Usage-Based Car Insurance in India 2025 rewards drivers who rack up fewer kilometres and avoid risky behaviour. If you want fairer pricing and don’t mind app-based feedback, UBI is worth a serious look. Compare options, read the data policy, and choose a kilometre slab that matches your routine.

Helpful tools and related reads on Bimatalk

- Car Insurance Premium Calculator

- 5 Car Insurance Add-Ons That Can Save You ₹2–3 Lakhs

- Third-Party vs Comprehensive—Which should you buy?

Last Updated on August 21, 2025 by Singh Sumit

2 thoughts on “Usage-Based Car Insurance in India 2025: Save Big with Telematics”