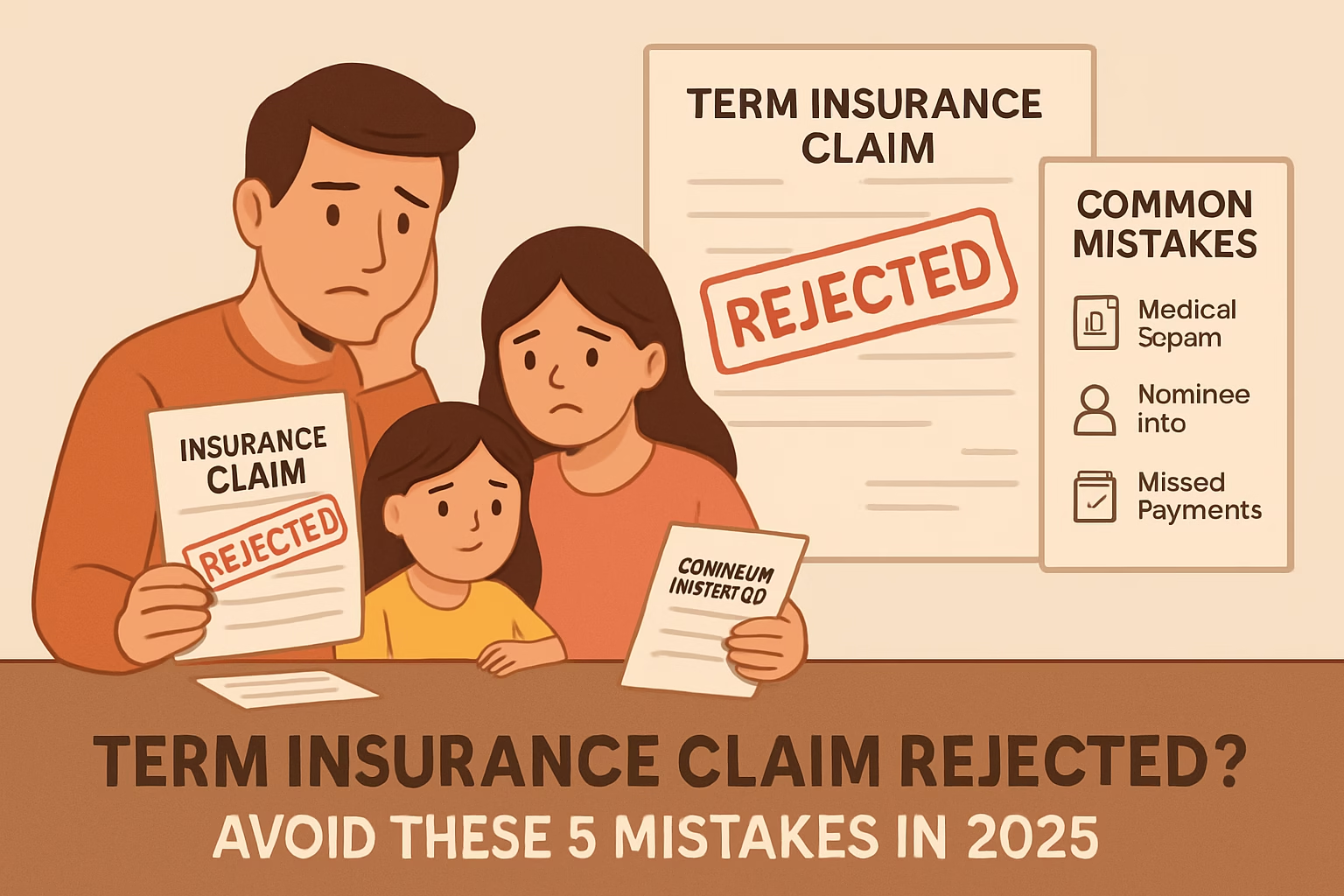

Term insurance claim rejection is a problem that many policyholders don’t think about—until it’s too late. You buy a term plan to secure your family’s future. However, if a claim is rejected, it can leave your loved ones helpless during a crisis. In this article, we will explore the main reasons why term insurance claims are denied. We will also share simple, smart steps you can take to prevent claim rejection.

1. 🧾 Providing Incorrect or Incomplete Information in the Application

Many people provide inaccurate information in their insurance application. They might do this to lower premiums or just by mistake.

Common omissions include:

- Smoking or drinking habits

- Accurate income details

- Family history of illness

- Previous hospitalizations or surgeries

❌ Why it leads to rejection:

Insurance companies conduct thorough investigations at the time of a claim. If any discrepancy is found between the information provided and their findings, the claim may be outrightly rejected.

✅ How to avoid this:

- Always declare everything truthfully, even if it increases your premium slightly.

- Submit accurate documents — income proof, ID, health reports.

- Ask your agent or online platform for help if you’re unsure how to fill something.

💡 Internal Tip: If you’re a working professional, check out our expert picks in Best Term Insurance Plans for Salaried Employees. You will find the perfect policy for your needs.

2. 🩺 Hiding Pre-existing Medical Conditions

This is the #1 reason why term insurance claims get denied in India.

Some buyers think that if they disclose their health conditions, their application will get rejected. These conditions include diabetes, asthma, and high BP. They also worry it will become expensive. So, they choose to keep it hidden.

❌ What happens:

Insurance companies verify hospital records, prescription history, and even diagnostic lab reports. If a major illness was hidden during the purchase, the insurer may deny the claim. It does not matter how long the policy was active.

✅ What to do:

- Go through a medical test even if it’s optional. It helps build trust with the insurer.

- Disclose every known medical condition, even minor surgeries.

- Choose insurers that are transparent about how they handle pre-existing conditions.

3. 📅 Letting the Policy Lapse Due to Missed Payments

Believe it or not, some families discover a harsh reality. They learn only after the policyholder’s death that the policy lapsed due to a missed premium.

❌ Why it leads to rejection:

If your term insurance is not active at the time of death, your nominee cannot claim anything. Even if you’ve paid for years, one missed payment can ruin everything.

✅ How to stay protected:

- Set up auto-debit with your bank.

- Use insurer apps that send payment reminders.

- Understand the grace period — usually 15 to 30 days after due date — and never let it pass.

4. 👨👩👧👦 Outdated or Incorrect Nominee Details

Your nominee is the person who will receive the policy amount. But many people forget to update this after marriage, divorce, childbirth, or the death of a nominee.

❌ What goes wrong:

If your nominee is no longer valid, your claim might be delayed. If your nominee is a minor without a guardian, your claim might be disputed.

✅ Smart tips:

- Review your nominee details every year or after major life events.

- Add a contingent (secondary) nominee if your primary nominee is unavailable.

- Clearly tell your family where the policy documents and claim process info are kept.

5. 📄 Claim Filing Errors or Delays

Your family may have the right to claim. However, they can still lose out due to paperwork errors. They might also miss out by filing too late.

❌ What causes this:

- Filing after the deadline (usually 30 days)

- Incomplete documents (death certificate, ID proof, medical records)

- Lack of knowledge about the claim process

✅ How to get it right:

- Educate your family about the claim process and documentation.

- Keep a copy of the policy and claim form with your nominee.

- Consider term plans with simplified digital claim filing like ICICI Pru, HDFC Life, etc.

📊 Best Insurers for Easy Term Claim Settlements (2025)

| Insurer | Claim Settlement Ratio | Key Benefits |

|---|---|---|

| HDFC Life | 99.39% | Life stage options, flexible payouts |

| Max Life | 99.51% | Critical illness, waiver on disability |

| LIC Tech Term | 98.52% | Government trust, online-only |

| Tata AIA | 99.01% | Whole-life cover, low rejections |

| ICICI Pru | 97.80% | Covers 34 critical illnesses |

📌 Final Advice to Avoid Term Insurance Claim Rejection in 2025

Here’s a quick checklist to ensure your family doesn’t face rejection:

- ✅ Disclose all medical and lifestyle facts honestly.

- ✅ Pay premiums on time.

- ✅ Keep your nominee updated.

- ✅ File claims on time and with complete documents.

- ✅ Choose an insurer with a strong reputation and high settlement ratio.

🧠 Final Words: Avoid Term Insurance Claim Rejection with Simple Steps

Buying a term insurance policy is a major step in protecting your family’s future. But it’s equally important to ensure that your policy is valid, updated, and free from risks of term insurance claim rejection.

Remember, your family shouldn’t suffer due to simple mistakes you can fix today. Be honest. Stay informed. Communicate with your insurer. Because a good policy is only valuable if the claim gets paid.

Last Updated on August 8, 2025 by Singh Sumit

Term beat

Thanks