Introduction: Why This IPO Is in the Spotlight

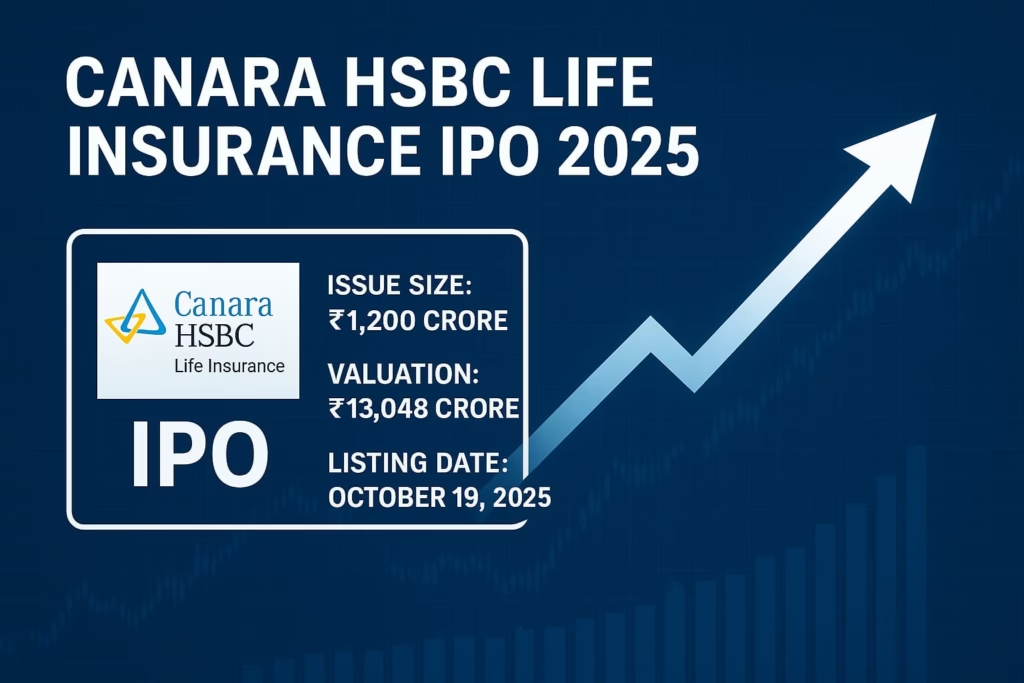

The Indian insurance sector is entering a new era of growth. Go Digit and Niva Bupa had successful IPOs. Now, investors have their eyes set on the upcoming Canara HSBC Life Insurance IPO 2025. The estimated issue size is ₹3,875–₹4,075 crore. The valuation is ₹16,500 crore. This IPO is not just another listing. It’s a signal of confidence in India’s booming financial services market.

But timing matters. This IPO comes at a moment when the global economy is rattled by Trump’s tariff policies. The Reserve Bank of India’s shifting stance on interest rates further destabilizes the market. Additionally, there is a sharp sell-off from foreign institutional investors (FIIs). On the domestic side, the GST cut on life and health insurance premiums (2025) is creating changes. It is reshaping how Indian households view insurance.

Put together, these factors make the Canara HSBC Life Insurance IPO not only a financial event. It also reflects India’s evolving insurance and capital market landscape.

About Canara HSBC Life Insurance and the Upcoming IPO 2025

Company History and Evolution

Canara HSBC Life Insurance Company Ltd. was established in 2008 as a joint venture between:

- Canara Bank (51%)

- HSBC Insurance (Asia-Pacific) Holdings (26%)

- Punjab National Bank (23%)

This partnership created a bancassurance powerhouse, allowing the insurer to leverage the branch networks of its parent banks while gaining global expertise from HSBC’s international insurance operations.

Product Portfolio

The company offers a diverse range of products including:

- Term insurance – Pure protection policies.

- Savings & investment-linked insurance – ULIPs and endowment plans.

- Retirement & pension products – Catering to India’s growing elderly population.

- Group insurance – Covering employees of corporate clients.

Market Position

Canara HSBC is smaller than giants like HDFC Life, SBI Life, and ICICI Prudential Life. However, it has carved out a strong position in the mid-tier insurance space. Its distribution strategy is anchored in bancassurance, which ensures a steady pipeline of customers.

IPO Details: Size, Valuation, and Timeline of Canara HSBC Life Insurance IPO 2025

- Issue Size: ₹3,875–₹4,075 crore

- Valuation: Approx. ₹16,500 crore

- Structure: Combination of fresh issue and offer-for-sale (OFS) by promoters

- Expected Timeline: September–October 2025, likely before Diwali

This timing aligns with the festive season, a period when Indians traditionally purchase financial products, including insurance.

Financial Performance Before the IPO

Revenue and Premium Growth

Canara HSBC has reported double-digit growth in its annual premiums over the last three years. A mix of term insurance sales and investment-linked policies has fueled this expansion.

Assets Under Management (AUM)

The insurer’s AUM stands at ₹25,000 crore, reflecting customer confidence and strong fund performance.

Profitability and Solvency

The company maintains a healthy solvency ratio, meeting IRDAI requirements. Profitability has improved steadily due to higher persistency rates (customers renewing policies).

Peer Comparison

- HDFC Life Insurance: ₹2.5 lakh crore AUM

- SBI Life Insurance: ₹3 lakh crore AUM

- ICICI Prudential Life Insurance: ~₹2 lakh crore AUM

- Canara HSBC Life Insurance: ~₹25,000 crore AUM

While smaller in scale, Canara HSBC offers a growth story with significant potential.

Key Factors Driving the IPO Market in 2025

The Canara HSBC IPO isn’t happening in isolation—it’s deeply connected to broader macro and policy factors.

Trump Tariffs: A Global Headache

The return of Donald Trump’s protectionist trade policies has sent shockwaves through global markets. Tariffs on steel, electronics, and other exports impact India’s IT, manufacturing, and financial sectors. Investors are therefore flocking to defensive industries like insurance, making this IPO well-timed.

👉 For a deep dive, read: Indian Market Factors 2025: Trump Tariffs, RBI Policy & FII Sell-Off

RBI Policy: Interest Rates in Focus

The Reserve Bank of India (RBI) plays a pivotal role in determining insurers’ investment income. Lower rates mean cheaper borrowing but reduced yields on insurers’ bond holdings. Conversely, if rates remain high, insurers benefit from higher returns on their investment portfolios. The market is closely watching RBI’s policy stance this quarter.

FII Sell-Off: A Double-Edged Sword

In 2025, Foreign Institutional Investors have been net sellers due to global uncertainty. While this has pressured Indian equities, domestic investors remain resilient, especially in IPOs. Canara HSBC’s offering may see strong participation from Indian retail and HNI investors, offsetting foreign outflows.

Policy Push: GST Cut on Life and Health Insurance

One of the biggest tailwinds for insurers in 2025 is the government’s decision to cut GST on life and health insurance premiums. The reduction is from 18% to 0%.

How Families Save More

For a household paying ₹50,000 in annual premiums, the GST cut results in savings of around ₹9,000 per year. This makes insurance more affordable for middle-class families.

Boosting Insurance Penetration

India has one of the lowest insurance penetration rates globally. By cutting GST, the government aims to make protection and health coverage more accessible. This is a long-term structural boost for companies like Canara HSBC.

👉 Learn more here: GST Cut on Life and Health Insurance Premiums 2025: How Policyholders Can Save ₹9,000 Annually

Investor Benefits and Risks of Canara HSBC IPO

Why Investors Should Be Optimistic

- Strong bancassurance partnerships with Canara Bank and PNB.

- Global brand credibility via HSBC.

- Favorable regulatory environment (GST cut, IRDAI reforms).

- Growing awareness of life and health insurance in India.

Risks to Keep in Mind

- Competition: Larger rivals like HDFC Life and SBI Life have bigger scale advantages.

- Regulatory Pressure: Pricing caps or stricter norms could affect margins.

- Market Volatility: Tariffs, interest rate shifts, and FII behavior could impact listing gains.

The Broader Impact on India’s Insurance Industry

The Canara HSBC IPO is not just about one company—it represents the maturing of India’s insurance sector.

- More private insurers may go public, boosting transparency.

- IRDAI reforms aim to improve customer-centric policies and digital adoption.

- The GST cut could accelerate the shift from underinsurance to adequate coverage.

Investor Perspectives

Retail Investors

- May find this IPO appealing for steady, long-term returns.

- Insurance stocks generally provide stable compounding.

High Net-Worth Individuals (HNIs)

- Likely to see it as a portfolio diversifier during market volatility.

Institutional Investors

- May evaluate based on long-term insurance penetration growth in India.

Expert Opinions and Market Sentiment

Market analysts expect healthy subscription levels, citing Canara HSBC’s strong parentage and growth potential. However, experts caution that listing gains may not be explosive. Insurance IPOs are better suited for long-term investors seeking stability. They do not favor short-term traders.

FAQs on Canara HSBC Life Insurance IPO

Q1. When is the Canara HSBC Life Insurance IPO 2025 expected?

Likely in September–October 2025, subject to SEBI approval.

Q2. What is the size of the Canara HSBC Life Insurance IPO 2025?

Between ₹3,875–₹4,075 crore.

Q3. What is the company’s valuation?

Around ₹16,500 crore.

Q4. Who are the promoters?

Canara Bank, HSBC Insurance (Asia-Pacific), and Punjab National Bank.

Q5. How does the GST cut impact this IPO?

By making insurance cheaper, the GST cut drives demand—strengthening Canara HSBC’s growth outlook.

Q6. Should retail investors apply for the Canara HSBC Life Insurance IPO 2025?

Yes, if seeking defensive, long-term growth in the financial sector.

Conclusion: Why the Canara HSBC Life Insurance IPO 2025 Matters

The Indian insurance industry is undergoing a massive transformation. Rising awareness and regulatory reforms are driving this change. There is also policy support such as the GST cut on life and health insurance premiums. Against this backdrop, the Canara HSBC Life Insurance IPO 2025 comes at the perfect time.

For investors, this IPO represents a chance to participate in the growth of a trusted insurer with strong parentage from Canara Bank, HSBC, and PNB. It offers exposure to a defensive sector that is less volatile than cyclical industries, making it a potential long-term wealth creator.

For policyholders and households, the GST cut ensures affordability, driving demand for insurance products. This, in turn, strengthens the business fundamentals of companies like Canara HSBC, boosting their growth trajectory post-IPO.

Market challenges such as Trump tariffs, RBI’s monetary policy decisions, and FII sell-offs will continue to influence short-term sentiment. Yet, the insurance sector remains resilient. The Canara HSBC Life Insurance IPO 2025 could benefit from this defensive positioning.

In short, the Canara HSBC Life Insurance IPO 2025 is both a milestone for India’s insurance market. It offers a long-term investment opportunity for those seeking stability, growth, and diversification.

🔗 External Reference: Times of India on GST reform

Last Updated on September 5, 2025 by Singh Sumit